April 11, 2024

Dear Great Lakes Wealth Clients, Families & Friends:

March was a month of new records. All three major equity indices — the S&P 500, Dow Jones Industrial Average and Nasdaq — hit all-time highs and equity markets were positive for the fifth month in a row. The equity market rally was driven by mega-cap tech stocks, the broadening of the market and optimism that the Federal Reserve (Fed) would deliver rate cuts later this year.

Bond yields were largely unchanged this month, sitting close to the upper end of their year-to-date range as the March rate cut didn’t materialize and the first rate cut now seems likely to happen in June or July. A record amount of issuance in investment grade corporate bonds was met with strong demand by investors as yields remain attractive even as credit spreads narrow.

The U.S. economy remains on solid footing, supported by strong job gains, improving housing activity metrics and growing consumer spending.

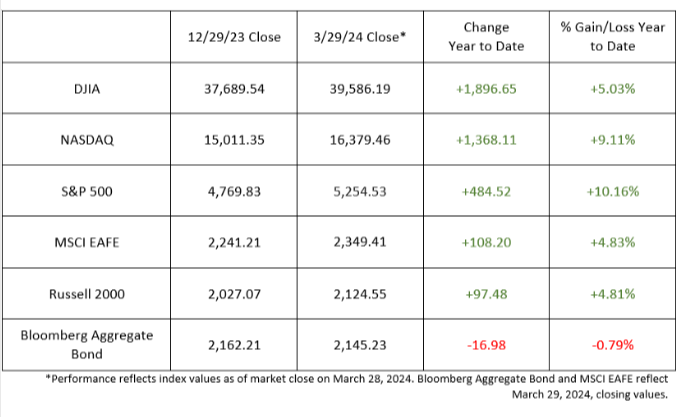

We’ll dive into the details below, but first, let’s review the year-to-date results:

Equity market optimism

Hotter than expected inflation data coupled with optimism regarding economic growth propelled commodity-related sectors, such as Energy and Materials, to outperform the index in March. Despite the upside inflation surprise, Fed Chairman Jerome Powell instilled confidence in the market during the Federal Open Market Committee (FOMC) press conference, reiterating the Fed’s commitment to remaining patient as inflation moves gradually toward its 2% target over time.

Although one 2025 rate cut was removed from the dot plot, the S&P 500 notched six new record highs in March as economic growth and employment were also revised favorably in the Fed’s Summary of Economic Projections.

Not much changed in fixed income

Despite some volatility, March offered little net change in Treasury yields. The exciting story remains in obtainable high-income levels for individual bonds as yields remain elevated in diverse products across the curve. Though the high-quality corporate curve is fairly flat, it boasts higher yields than have been available for nearly two decades. Longer-term municipal yields benefit from an upward-sloping curve from 15-30 years in maturity, providing attractive taxable-equivalent yields for high earners.

U.S. economy keeps chugging along

The February Leading Economic Index, a general indicator of where the U.S. economy is heading, was positive for the first time since February of 2022. The U.S. service sector continued to expand in February, industrial production was slightly positive and higher than expected, with construction as well as business equipment production driving the Index higher. Housing market indices were mixed, with existing home sales surging among higher available inventory and new home sales decreasing during the month. Nonfarm employment increased by 275,000 in February, but the strong January number was revised considerably lower, netting 167,000 fewer jobs than originally reported.

D.C. to weigh defense and tax packages

Following the passage of all 12 government funding bills in March, attention in D.C. has turned to the potential passage of the $95 billion defense supplemental and the $78 billion tax package. House Speaker Mike Johnson (R-LA) has indicated he will bring the defense package to the floor for a vote after the Easter Congressional recess. While the passage of the tax bill would represent a market positive for capital- and R&D-intensive businesses and discretionary income for low-income families, ongoing Senate disagreements around the Child Tax Credit and an increasing desire to defer tax negotiations to 2025 continue to weigh on its prospects.

Ukraine becomes adept at targeting Russian oil refineries

While the Kremlin has not tried to weaponize its oil industry the way it tried (and failed) to weaponize natural gas, the last month provided a reminder that the war in Ukraine can still affect the oil market. Though Ukraine lacks the ability to strike Russian oilfields, which are typically located in Siberia – too far for drone strikes – it has successfully damaged at least seven refineries around Russia, hundreds of miles from the front line. It’s worth noting that Russia started the practice of targeting energy infrastructure during the winter of 2022-23, damaging numerous Ukrainian power plants.

Has the global economy turned a corner?

International equity markets have continued to drive higher as the dollar has strengthened against most major currency pairs. The latest round of developed markets’ “risk-on” price action follows updates from significant central banks that policy loosening is now imminent and the growing belief that the global economy has turned an important corner.

The most significant monetary policy development proved to be the Bank of Japan’s exit from negative interest rates for the first time in eight years. Japanese investors are among the biggest exporters of capital in the world, borrowing in cheap yen to invest in higher rate destinations elsewhere, including the United States.

Of greater surprise is the Swiss National Bank’s cut to that country’s key interest rate by 0.25% to 1.50%, a signal to others in the euro zone of easier monetary policy to come. The Bank of England has sent a strong signal that rates are very likely to start falling in the UK as well in response to an anticipated easing in inflationary pressures – probably in June.

The bottom line

By the end of 2024, we expect a slowing of economic growth in the United States, but not a recession.

• We expect U.S. equities to be volatile in the short-term, but to be positive in 2024. Do you remember the old saying, “Sell in May and Buy back after Labor Day”?

• We believe that interest rates have peaked and may fall in the second half of 2024.

• Cash is king, and Bonds are back. We would add traditional fixed income, particularly money markets and short dated bonds, for safety and stability in 2024.

• We recommend investors to continue to consider an overweight of alternative investments, including private equity and debt.

• Gold has broken through $2,300. We expect to see continued higher prices, and have raised our target to $2,500 per ounce, in 2024.

• Cryptocurrencies have soared in 2024. Bitcoin is now above $68,000 per coin, reaching its highest point since 2021. We expect continued volatility.

• Depending on your timeframe, current investment strategies should be based on what’s happening “Now,” “Next,” and “Later.”

• We currently have a “Buy” on 11 of our 12 strategies. Which strategy is right for you? That just depends on your risk tolerance, ultimate objective, etc. We are happy to discuss this with you.

• Our current approach continues to be discipline and patience when both buying and selling. Volatility will continue to create opportunities for 2024.

The equity market’s strong start likely increases the likelihood of near-term volatility. It typically experiences three to four pullbacks of 5% or more each year and hasn’t had one since September 2023. But long term, our overall outlook remains positive.

As ever, we remain committed to the pursuit of your financial goals. If you have any questions regarding this recap – or any other topic – we will be happy to review & discuss them on our next scheduled call. Thank you for your continued trust in Great Lakes Wealth. We look forward to speaking with you soon!

Sincerely,

Your Investment Team at Great Lakes Wealth

Investing involves risk, and investors may incur a profit or a loss. All expressions of opinion reflect the judgment of the Raymond James Chief Investment Officer and are subject to change. There is no assurance the trends mentioned will continue or that the forecasts discussed will be realized. Past performance may not be indicative of future results. Economic and market conditions are subject to change. The Dow Jones Industrial Average is an unmanaged index of 30 widely held stocks. The NASDAQ Composite Index is an unmanaged index of all common stocks listed on the NASDAQ National Stock Market. The S&P 500 is an unmanaged index of 500 widely held stocks. The MSCI EAFE (Europe, Australasia and Far East) index is an unmanaged index that is generally considered representative of the international stock market. The Russell 2000 is an unmanaged index of small-cap securities. The Bloomberg Barclays US Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. An investment cannot be made in these indexes. The performance mentioned does not include fees and charges, which would reduce an investor’s returns.Investing in the energy sector involves special risks, including the potential adverse effects of state and federal regulation, and may not be suitable for all investors.A credit rating of a security is not a recommendation to buy, sell or hold the security and may be subject to review, revision, suspension, reduction or withdrawal at any time by the assigning Rating Agency. Bond prices and yields are subject to change based upon market conditions and availability. If bonds are sold prior to maturity, you may receive more or less than your initial investment. Income from municipal bonds is not subject to federal income taxation; however, it may be subject to state and local taxes and, for certain investors, to the alternative minimum tax. Income from taxable municipal bonds is subject to federal income taxation, and it may be subject to state and local taxes.Investing in commodities is generally considered speculative because of the significant potential for investment loss. Their markets are likely to be volatile and there may be sharp price fluctuations even during periods when prices overall are rising. International investing involves special risks, including currency fluctuations, differing financial accounting standards, and possible political and economic volatility. The companies engaged in the communications and technology industries are subject to fierce competition and their products and services may be subject to rapid obsolescence. The Consumer Price Index is a measure of inflation compiled by the US Bureau of Labor Studies. The Leading Economic Index (LEI) provides an early indication of significant turning points in the business cycle and where the economy is heading in the near term. Material created by Raymond James for use by its advisors.